Can GoPro 📸 Be A Hero?

Breaking down the challenges & opportunities with $GPRO stock

Happy Trade War Talks week! Maybe this is finally the week where the US and China get an actual agreement in place (I doubt it). But since there’s plenty of ink already spilled on that, I want to talk about something else that’s arguably more actionable.

People often ask me, “where can I find good stock ideas?”. There’s a TON of places to find potentially interesting stock ideas, from running qualitative & quantitative screens, monitoring SEC filings, following the positions & filings of certain investment funds, picking up on legal insider transactions, reading websites like SeekingAlpha or the Wall Street Journal, looking at new & recent IPOs, searching through news or transcripts for specific keywords, watching price % losers/gainers and 52 week high/low lists, doing competitor or industry research, following certain accounts on Twitter, and even just picking up on major consumer trends in one’s daily life (the old Peter Lynch method!). [Quick shameless plug: I cover many of these areas / tactics in depth in my courses and in weekly videos over at the subscription-based Skill Incubator Wealth Building Community]

To me the two MOST important keys 🔑🔑 to consistently having a healthy funnel full of potential stock ideas are 1) READ A LOT and 2) BE CURIOUS as hell all the time. Great stock pickers typically love the process of hunting for needles in the haystack. We are information junkies who scour lots of sources but who also develop a good filter for what’s noise and what’s signal, similar to great investigative journalists or detectives. Personally I’m constantly adding to ➕ and subtracting from ➖ some very long watchlists of stocks while waiting for the right catalysts / prices to strike on the most compelling of the bunch. It’s like Warren Buffett famously said, “there are no called strikes in the business”. Investors can wait and wait and choose to act only on the truly best opportunities. And I keep working hard in the meantime to find them.

A Tweetstorm Gets The Wheels Turning 💡

So that said, I came across an interesting Twitter thread and blog post this past weekend that got me re-engaged with a stock that has crossed my watchlist a few times but never made the cut as an investment. The stock is GoPro ($GPRO) and the Tweetstorm is from a guy I’ve never met. But this dude, Adam Keesling, seems pretty smart and likes to analyze consumer companies’ business models which is candy to a stock geek like me. Adam’s Tweetstorm (see below) walks through the recent past of GoPro, the action sports camera company which IPO’d at a $3 Billion dollar valuation back in June 2014:

Now as Adam mentioned, $GPRO has been an abysmal stock, losing over 90% of its value from its post-IPO peak nearly five years ago 😳:

Adam talks about some of the reasons behind the poor performance, including:

A very high post-IPO valuation that depended on mass market adoption

A shift to marketing to a mainstream audience in an attempt to meet those aggressive growth expectations (alienating some core action-sports customers)

The hiring of expensive high-profile media executives to build a content business

Poor execution with the Karma Drone product (now abandoned)

Camera hardware = infrequent purchase for most consumers

Adam’s points are pretty much spot-on, though he misses a few notable things. His prescription for GoPro is for the company to use their camera sales as a wedge to sell more high margin software. He briefly acknowledged that GoPro has already been heading in this direction since 2016 when they bought two video editing apps, but thinks they can do more with services & software to become a platform to help influencers manage & scale their fanbases.

The last point is an interesting one, and I happen to agree that software & services is an area that GoPro might be able to derive value from. More on this a little later!

The timing of Adam’s post was serendipitous as it coincided with another dramatic sell-off in $GPRO last week, after the company announced about a 1.5 month delay in shipping its new HERO8 cameras along with a small cut to its full year financial guidance. The stock was down 20% on the announcement:

Now GoPro will still have its new cameras on shelves for the crucial holiday selling season, so the slight delay doesn’t seem like THAT big of a deal in the grand scheme. However, the company has a history of disappointing investors so it gets punished heavily for any small infraction.

I noticed that $GPRO now sports a market cap of about $550 million and trades for a roughly 10X Price-to-Earnings multiple using their updated 2019 earnings guidance. That’s not terribly expensive but it might not be cheap either, depending on future growth and cash flow generation. I like to take a look at stocks that the market has become ultra-pessimistic about to see if there’s possible hidden value above-and-beyond just a low valuation. Is there hidden potential value in $GPRO?

First, The Bear Case 🐻

Adam touched on some reasons for GoPro’s stock bloodbath over the past few years, but here’s some additional things he skipped over:

Smartphone cameras have gotten insanely good over the past few years which has limited GoPro’s appeal to the broad mass market consumer

Even in action sport cameras, GoPro faces fierce competition from DJI

GoPro’s annual revenue peaked in 2015 then declined in 2016, 2017, & 2018

GoPro’s gross margins have steadily declined due to discounting & lower selling prices. GPRO’s 2018 gross profit is down roughly 46% since 2015

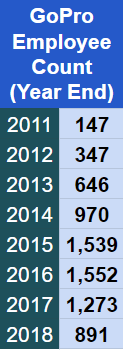

GoPro over-hired in many areas of its business (not just media) and its cost structure was too bloated, leading to net losses in 2016, 2017, & 2018 (see below)

GoPro has about $50 million of net debt on its balance sheet, and burns cash in most quarters (typically those lacking a new product launch). Cash burn isn’t sustainable long term, especially with a large debt repayment looming in 2022

GoPro’s CEO Nicholas Woodman seems to have a poor reputation with investors, many of whom blame him for the company’s product delays & missteps and criticize him for his frequent stock sales to fund his lavish lifestyle which includes owning yachts and private aircraft

Shareholder governance at GoPro is problematic. Nicholas Woodman has super-voting shares and the company is also a prolific issuer of stock options & RSUs, which dilutes existing shareholder stakes over time. The company has 31 MILLION shares available for future grants (20% of the company) and that number grows each calendar year due to an AWFUL evergreen grant program similar to the one I wrote about last week with Stitch Fix

So What’s To Like? 🤔

Here’s where the eternal optimist in me gets to shine!

If you were paying attention to the charts above, you might have noticed that GPRO’s annual losses have been improving each year for the past three years. The company has been cutting headcount and overhead costs, and actually expects to grow revenue AND turn a profit this year. Current earnings per share guidance for 2019 is in the $0.33-$0.39 range, which is how we get that ~10X P/E multiple I mentioned previously. Management also expects positive cash flow and for the company to be in a slight net cash position by the end of the year (cash > debt).

That’s all fine, but doesn’t get me super excited. There are plenty of cheap stocks in this market, many trading at single digit earnings multiples, with proven management teams and better track records of shareholder value creation. It’s a start though, and more importantly it may give GoPro time & runway for a comeback.

That POTENTIAL comeback story I see with GoPro lies in 3 KEY 🔑 AREAS:

Software (Video Editing etc)

Subscriptions (GoPro PLUS)

HERO8 opening up large adjacent hardware market (Vloggers, Influencers, etc)

The Opportunity in Software 💾

Woodman & Co actually deserve some credit for seeing the software opportunity a couple years ago when they acquired a pair of video editing apps in early 2016. At a cost of $105 million, I think they probably overpaid for those assets, but perhaps it will work out longer term. Video creation & consumption continue to explode globally, and will continue to for the foreseeable future as smartphone cameras and 5G wireless availability keep improving.

While Instagram, Bytedance (TikTok), Twitter, Facebook, and Snapchat soak up a lot of short-form video where minimal edits can be made in-app, the number of longer videos requiring more advanced editing continues to grow as well. From YouTube to online courses to company marketing and beyond, editing outside the walled garden apps requires good software and expertise.

This is one of the primary reasons that Adobe ($ADBE) boasts a market cap of around $134 BILLION and has seen its stock rise over 300% in the past five years:

That’s a nice looking chart if you’ve been an $ADBE shareholder! Creative Cloud, which is the suite of photo and video editing software (cloud-based) produced by Adobe, currently produces about $6.6 billion of annual revenue with gross margins of over 95%! 😮

That product alone makes up almost 60% of Adobe’s annual revenue and an even higher percentage of gross profit. It’s probably safe to say that Creative Cloud accounts for at least $70 Billion of Adobe’s market cap, and if it were a standalone business it would have a Price-to-Revenue multiple greater than 10X.

Now imagine for a second that GoPro could capture and monetize some of that growing video editing market in the near future. For every 1% of Adobe’s current revenue that GoPro captures, assuming 80% gross margins, that would add about $50 million of annual gross profit to GoPro’s financial results. Most of that would likely translate to incremental net profit, so it’s not crazy to think that GoPro could see an uplift of $.30-.35 in per share earnings ($50 million / 155 million shares outstanding today) for every 1% of market share capture. That’s the size of 2019 EPS today! If GoPro captured just 3% of the market it might increase EPS to more than $1.30 per share, or 4X current levels. Today Adobe trades at a 30X forward P/E multiple. If $GPRO were to achieve EPS of just $1.00 per share and garner a P/E multiple that is just HALF of $ADBE’s, then $GPRO stock would trade for ~$15 per share or over 4X today’s price!

To $GPRO’s credit, management understands the opportunity. Here’s some of their recent comments that I found searching through conference call transcripts:

Now how likely is it that $GPRO pulls it off? Today the market puts a VERY low probability (essentially zero) on GoPro getting market share. That feels right today. Adobe’s software is very robust and widely recognized as the industry leader. They have large teams of developers pumping out improvements and new versions all the time. But the video editing software market is large and still growing nicely (26% YoY growth for Adobe last quarter). Competitors such as Final Cut Pro (Apple), iMovie (Apple), Windows Movie Maker, Camtasia, Vegas Pro (MAGIX), Avid Media Composer, and others generate meaningful revenue in this market.

Today GoPro is not a major player in that market BUT there’s a case to be made that they have a shot to carve out some market share on mobile devices. On iOS, the GoPro app’s download ranking in the US Photo & Video category has recently fluctuated between 75 and 100, and maintains a solid 4.8 star rating:

In the free app category, I counted at least 20 video editing apps that outrank GoPro’s app. So that’s not great. Despite a good review score, GoPro needs to climb the ranks.

In the Google Play Store, the opposite is true. GoPro appears to have a relatively poor user review score (2.7), but ranks higher in its category (mid 40’s ranking):

None of that looks super compelling. HOWEVER, GoPro does outrank Adobe’s Premier Rush app, which is their fresh product aimed at simplifying and making video editing more accessible. Rush is slightly behind on iOS and far behind on Google Play. Might an aggressive competitor of Adobe be interested in acquiring GoPro as a beachhead for a competitive assault? Or Adobe itself to play defense? Perhaps 🤷♂️

More realistically, if GoPro can successfully get cameras into the hands of more consumers, that could drive higher uptake of GoPro’s editing software as well. The new HERO8 product is actually another shot at expanding the addressable market for GoPro cameras which I’ll cover shortly.

As Adam mentioned, perhaps there are other software niches GoPro can tackle as well, though I don’t see evidence of those efforts currently.

The Opportunity In Subscriptions 💸

Three years ago (in mid 2016) GoPro launched their monthly subscription service called GoPro PLUS. That service now costs ~$5 per month and gives subscribers:

unlimited cloud storage for GoPro footage

free or discounted replacement of damaged GoPro cameras

discounts on GoPro gear & accessories

It’s like Dropbox + AppleCare + membership rewards for GoPro camera owners. And it’s very high margin recurring revenue for GoPro that has the potential to drive significant earnings if the company can attract enough subscribers:

So $GPRO’s CFO is on record saying one million GoPro PLUS subscribers would mean $0.30+ in additional earnings per share (doubling of current EPS). Today $GPRO has roughly 250,000 GoPro PLUS subscribers, with that base growing at roughly 50% year-over-year in the most recent quarter. Given that growth rate, half a million subs seems achievable within 3 years, even if the growth rate decelerates modestly. One million subscribers might take anywhere from 3-10 years (or never) depending on the growth rate acceleration/deceleration as well as churn rate.

GoPro expects to sell more than 4.3 million camera units this year, and has cumulatively sold over 30 million cameras in the last decade. There’s likely 10-15 million active camera owners and growing, so 1 million subscribers would be somewhere in the neighborhood of 5% take rate. I’ve seen anecdotal data suggesting that’s roughly at the level of AppleCare uptake, and Dropbox has about 3% paying users (as a % of total active users) despite a price point that’s more than double GoPro PLUS. Other premium subscription benchmarks roughly align with these figures and suggest 5% take rate is potentially achievable.

The Opportunity With New Hardware (HERO8) 🎥

For now, the #1 thing GoPro can do to drive success in software & subscriptions is continue to produce and sell great cameras. The more consumers that join GoPro’s ecosystem, the better. GoPro’s new HERO8 camera looks like it might be a step in the right direction, because it stays true to its action sports roots while offering new features & attachments aimed at attracting a broader audience.

People who get serious about recording video eventually go down the rabbit hole of buying expensive gear to improve audio quality, lighting, and details like resolution/focus/transitions/etc. High end smartphones have good capture resolution but really fall short when it comes to lighting and sound in particular.

GoPro’s HERO8 introduces new hardware add-ons specifically aimed at improving lighting and audio, along with a display aimed at vloggers who shoot selfie style:

This isn’t going to cause professional videographers to ditch their DSLRs, lenses, tripods, box lights, hot shoes, and wireless mics. But it’s possible that it could attract some new influencers and video creators who are just getting into the game. It’s a much simpler and cheaper (~$600 for camera + all mods) solution for those starting out. And it comes with all the other bells & whistles GoPro is known for, like mounting, 4K, 1080p, waterproofing, image stabilization, voice control, timers, etc.

A friend of mine with 200K+ YouTube subscribers even texted me:

“this looks like a game changer…likely to crush dslr’s with the vlogging crowd”

It’s certainly a strong effort to expand GoPro’s appeal, which it desperately needs. Shooting and editing high quality video are truly daunting and time-consuming tasks, so if GoPro can simplify these tasks with hardware and software solutions then it’s a win for everyone involved.

Anything Else? 😴

If you aren’t yet asleep, bless you. There’s just a couple other things worth noting before I finish.

GoPro is a widely recognized brand with a relatively high Net Promoter Score. It failed at creating an entertainment & media business a few years back, but it has succeeded greatly in attracting followers on social media:

📺 YouTube: ~8 million followers and 40+ million monthly views

📷 Instagram: ~16 million followers

📘 Facebook: ~11 million followers

GoPro and its users produce some unbelievably epic video footage. GoPro even has a partnership with Adobe to provide videos for Adobe Stock. Might this content & community be worth something to one of the big media conglomerates or streaming companies that are currently buying up content rights left and right? Or perhaps a social media company like Snapchat that’s fighting to stay relevant? Maybe an action sports associated brand like RedBull? Or even an iconic consumer hardware & software company that dabbles in GoPro’s markets, has boatloads of excess cash, and has made acquisitions of consumer hardware brands before? It isn’t a crazy thought.

When it comes to management, I’ll leave it to you to decide your opinion on the founder CEO Nicholas Woodman. He’s done some questionable things but he’s done some decent things too. In 2018 the Board cut his salary to $1 and he was not eligible for a bonus. Sadly, as of 2019, he’s back to an $800K base salary and 100% potential bonus despite the stock being down from where it started 2018! Although Woodman started selling a bunch of his stock in early 2019, it appears he may have paused after June. He still owns around 27 million shares (~17% of the company). There’s a lot of confusing signals here when attempting to figure out his alignment with shareholders.

One thing that really bothers me is the share dilution and ever-increasing amount of shares available for grants to GoPro employees. Woodman and his Board simply cannot allow that to continue. Employees and execs should not be rewarded year after year while the stock sinks. No more issuing shares and options with lower strike prices, enough is enough. It’s time for management to step up and deliver returns to shareholders. It’s in management’s own interest from a financial and reputational standpoint anyway.

TL;DR (THE END) 👋

GoPro’s stock price is currently at it’s all-time low. The company has had numerous missteps over the past four years, and it may even face extinction if it fails to generate better financial performance. However, there’s also a LOT of optionality and potential catalysts lurking within GoPro. The company is trending in the right direction with improving financial results. If it can gain momentum in its hardware, software, and subscriptions, it has the potential to be a multibagger stock.

For me it will be almost as interesting watching what happens 🍿 as watching this: