Mispriced Optionality (Part 1 of 2)

Why a select portfolio of pre-deal SPAC warrants might be compelling

Surprise! You probably thought this newsletter was dead. I apologize for not writing here since 2020. Thankfully there’s been an explosion of great investment newsletters in my absence. My own intention is to write more in 2022 and beyond. I believe there’s still a need for thoughtful investing content online, particularly serving the individual investor. We’ll see how I progress going forward. Thank you to those of you who choose to stick around.

The TL:DR

On to today’s topic: pre-deal SPAC warrants. I personally believe a number of them are significantly underpriced. The risk-reward looks asymmetric and tilted to the upside in my opinion. I aim to illustrate the potential opportunity here.

[Disclaimer: I personally own a portfolio of select pre-deal SPAC warrants. Warrants are risky and have the potential for loss. I have done my own diligence and accepted the risks. Your investments are your responsibility alone. The intent of this post is education and not investment advice.]

Current Background on SPACs

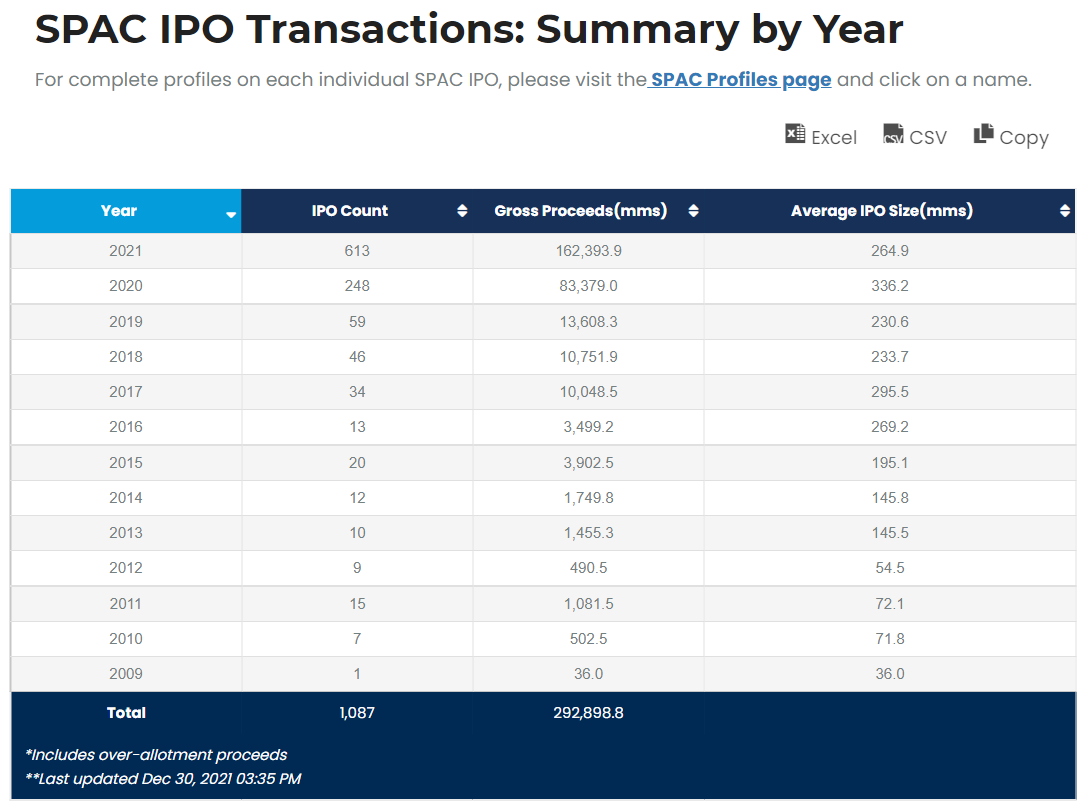

If you aren’t familiar with SPACs (special purpose acquisition companies), have you been living under a rock? 😁 I kid. These “blank check” companies have existed for a long while but SPAC fundraising boomed in 2020 and 2021. SPACs raise capital with the intent of using that capital to buy into a private company and take it public via the SPAC’s own public listing. There are many nuances to this process which are beyond the scope of this piece. The amount of capital which has flowed into SPACs within the past two years is stunning (nearly $300 Billion raised!):

Over 250 companies have successfully completed SPAC transactions and gone public through SPAC deals in the past two years. SPACs have become an alternative route to going public and in conjunction with a strong traditional IPO market have helped reverse the decade long trend of a shrinking universe of publicly traded US stocks. That’s the positive viewpoint. The negative viewpoint is that SPACs have allowed many low quality companies to come public despite weak financials, overly optimistic future projections, and general unsuitability for public markets.

The performance of deSPACs (companies that have completed their going public transactions via SPAC) in 2021 has been rather abysmal on average. One way to visualize this is to check out the chart on the $SPAK ETF, which holds a portfolio of mostly deSPACs, over the past year:

There are plenty of positive performances among completed SPACs such as Vertiv, Lucid, DraftKings, BeautyHealth, Matterport, MP Materials, etc. But there are many others which have quickly traded well below the initial SPAC deal valuation (typically calibrated to an initial $10.00 per share price), including such gut punchers as Talkspace, Metromile, Beachbody, CarLotz, Clover Health, AppHarvest, Desktop Metal, and ATI Physical Therapy. All of the latter are down 50% or more from their initial deal price. The deSPAC universe now sports a negative return from inception!

Another concerning issue in SPAC world is that there are almost 700 SPACs with $200+ Billion of capital competing for the pool of companies willing & ready to go public via this non-traditional route. Recent deSPAC performance has been poor and professional investors have been increasingly pulling their capital out of SPAC deals before the deal completes (via redemptions and/or de-committing from PIPEs). This reduces the capital available to a target company upon completion of a deal, which is not ideal for companies needing growth capital alongside their public market debut. It sows doubt in the minds of private company management teams. It seems likely that the target company pool is shrinking at the worst possible time for SPACs.

Did I mention the clock is ticking for SPACs still seeking a deal? Most SPACs have a 1-2 year window to complete a deal or else they are obligated to wind down and return their initial investors capital. A significant portion of existing SPACs have deadlines approaching by mid 2023:

In 2021, there were typically 15-20 SPAC deal announcements per month, though there were as many as 40 (February ‘21) and as few as 10 (October ‘21) in a given month. At the average pace of around 20 per month, 240 deals per year would be announced. One or two announced deals are terminated each month however, and that number appears to be rising in late 2021 (four terminations in December ‘21). That leaves about 150-200 deals completed annually at the existing rates. With more than 600 new SPACs raised in 2021, only about half of the 2021 SPAC class would complete deals within a two year window at the current pace. I very much agree with Andrew Walker of Yet Another Value Blog (a fantastic investment newsletter & podcast in my opinion) who has predicted rising SPAC liquidations in 2022.

Background on SPAC Warrants

Given these dynamics, why on earth would I see opportunity in pre-deal SPAC warrants?

Let’s first get the basics of SPAC warrants out of the way. Warrants are essentially long term call options, and therefore a leveraged bet on underlying stock performance. With SPACs, warrants are sold to both insiders and investors in the SPAC IPO at prices typically ranging from $1.00-1.50 per warrant. Most SPAC warrants have an exercise price at $11.50 per underlying SPAC share which allows the holder to acquire underlying shares for $11.50. Recall that SPAC shares are usually sold at $10.00 per share and the number of shares sold varies based on how much capital the SPAC is raising. Therefore, a strong performing deSPAC stock that goes up to say $15+ would make the option to acquire shares at $11.50 pretty darn valuable! SPAC warrants typically have a five year term that starts ticking after an initial business combination deal is consummated by the SPAC. One of the most important features of SPAC warrants is that they expire worthless if the SPAC winds down without completing a deal.

There are other wrinkles to SPAC warrants, including the ability for the company to redeem the warrants from their holders early if a deal is completed and the underlying deSPAC company shares reach a trigger price for a certain amount of time (typically $18.00 per share for 20 out of 30 trading days). In most of these redemption scenarios, the warrants would be worth multiples of their initial sale price, despite the holders losing out on future upside.

You can imagine that a five year call option on a stock, particularly a stock with high volatility and/or growth potential, is pretty valuable even when that call option is not yet “in the money” (underlying stock not yet trading above the option exercise price). With traditional listed call and put options, the longest term an investor could buy an option for is typically just 2-3 years out into the future. For example: if you want to buy a call option to purchase Apple stock at a level slightly higher than where it trades today, expiring in early 2024 (~ 2 years from now), it’s still going to cost you a sizable outlay. That’s due to “optionality” or “time value” which makes the option worth something today given reasonable probability of the stock being much higher in two years time. And that is despite the fact that there is non-zero probability that the underlying Apple stock could be lower over the next two years and therefore the option can expire worthless (100% loss of purchase price). The important thing to understand is that warrants, which are similar to five year call options, can have significant value due to future potential performance of underlying stock.

SPAC warrants typically start trading publicly soon after a SPAC raises its initial capital, before any deal with a target company is reached. Given 600+ existing SPACs are still out there seeking deals, there are hundreds of “pre-deal” SPAC warrants currently trading on public exchanges. As of 12/30/2021, pre-deal SPAC warrants are trading at a median value of $0.70 per warrant (average ~$0.90 per warrant) by my calculations. Nearly 500 pre-deal SPAC warrants trade below $1.00 per warrant and almost 200 pre-deal SPAC warrants currently trade at $0.60 or below.

The Opportunity in SPAC Warrants

Are some of these pre-deal SPAC warrants cheap/underpriced? We know most of them currently trade below their initial purchase price ($1.00-1.50) where insiders and institutional investors purchased them. But where should they trade and what is the potential upside in a successful SPAC deal scenario? I’m going to tackle this from several angles:

Theoretical option pricing models (Black-Scholes, Monte Carlo simulation, etc)

Actual historical performance of warrants with successful SPAC business deals

This will get in the technical weeds for a few minutes but stick with me and I think it will make sense.

Option Pricing Models

The Black-Scholes-Merton (“BSM”) model is the most widely known model for pricing simple call and put options. It’s most critical inputs include option exercise (“strike”) price, time to option expiration, current underlying stock price, and underlying stock volatility. It’s not the most accurate option pricing model out there and it can’t account for exotic features in options, but it’s not bad for giving ballpark price estimates for some options. If we ignore the complexity of SPAC warrant features, we can use BSM to get a ballpark estimate of what a five year call option would be worth on day 1 for a SPAC that has completed a business combination with its target. [Note: I assume 45% annualized stock volatility despite many recent deSPACs displaying annualized volatility above 50%]

With the underlying SPAC stock at $10 (and assuming a consummated business deal), the simple five year call option would be worth about $3.61. Now we know many SPAC warrants can be forcibly redeemed once the underlying stock trades above $18.00 for about a month. Giving up some upside optionality above $18.00 on the underlying stock is sort of similar to selling a call option at that strike. Using the same inputs as before, but an $18.00 strike price, we get to a $2.34 value for that call option:

Thus a buyer of a five year call struck at $11.50 who is giving up their upside above $18.00, might be willing to pay a net cost of $1.27 ($3.61-$2.34). Paying $1.27 for this option spread is surprisingly close to what insiders are actually paying for SPAC warrants upfront when SPACs raise initial capital. It’s also well above where most pre-deal SPAC warrants are currently trading.

However, there are multiple problems with using Black-Scholes approximations to price SPAC warrants. The BSM model is used for “European style” options that can only be exercised at expiration, yet SPAC warrants can often be exercised “American style” at any time after deal completion (which makes them more valuable). Furthermore, I way overestimated the option value hit from the warrant redemption feature in the paragraph above. The warrant redemption feature does not necessarily lead to giving up all upside above $18.00 per share, as the underlying stock must trade above that level for 20 out of 30 trading days, during which time the warrants can be exercised or sold to capture upside before redemption. The true value hit from the redemption feature is a fraction of the previous estimate and therefore the value of SPAC warrants at deal completion is theoretically higher than $1.27.

So given the complex/exotic nature of SPAC warrants, is there a better valuation model? Yes, sort of. Complex options do not have simple pricing equations (closed form solutions), but approximations and simulations are used. Most accounting firms that work with SPACs utilize Monte Carlo simulation to value warrants. I’m not going to bore you with the details, but I put together my own Monte Carlo simulation model in Python. I’ve run tens of thousands of simulations and the average warrant value tends to end up around $2.90 (with the SPAC stock trading at $10.00). I don’t believe there are any obvious errors in my code, but please let me know if you spot one.

If the value of an average SPAC warrant should theoretically be $2.90 on the day the SPAC completes a deal, but pre-deal SPAC warrants are trading at an average of $0.70, that would seem to imply the market believes the liquidation rate going forward will average about 76% (expected value calc here is 76% x $0.00 + 24% x $2.90 = $0.70). Historically the SPAC liquidation rate has been less than 10% judging by the data from S&P, spactrack, spacinsider, and spacanalytics. In fact there were only a few SPAC liquidations in the past several years. I said earlier that I do expect the number to increase going forward…but is 76% the correct figure? I doubt that.

Real World Warrant Returns

It’s interesting to look at the current & historical warrant prices of SPACs that have completed business combinations in the past two years, of which there are roughly 260 based on the data (via spactrack.io). Not all SPACs have warrants, and historical pricing on warrants is not widely available, but I’ve been able to get historical warrant prices for about 230 of these SPACs through my own stock price database.

Today the median post-deal SPAC warrant price trades around $1.15 (average is ~$1.60). This understates the potential for warrant upside since 1) it excludes the best historical performers whose warrants were redeemed at high prices (in many cases between $5.00-$20.00 per warrant) and 2) warrants have generally sold off in the past two months because of seasonal tax loss selling as well as current negative sentiment towards deSPACs. If I include redeemed warrants in my calculations at their prices just prior to redemption (not all time highs), the median post-deal SPAC warrant rises to ~$1.40 and the average balloons to ~$2.70. Roughly one-third of post-deal warrants trade above $2.00 or were redeemed above $2.00. Almost two-thirds trade above $1.00 or were redeemed above $1.00. Using all time high prices or prices from earlier in the year would skew things further to the upside. Either way, these numbers are closer to the theoretical warrant values from the Monte Carlo simulations and much higher than today’s average pre-deal warrant prices.

It is also insightful to look at warrant prices just prior to and just after SPAC deal announcements this past year. This was a difficult data set to wrangle, but I did it manually for you dear readers. Here’s a link to the raw data in Google Sheets. The median price of warrants just after deal announcement was $1.30 in 2021, with a median percentage change of 15% on deal announcement. Averages skew much higher due to outliers such as DWAC, CCIV/LCID, ACTC/PTRA, CAPA/QSI, etc. Here’s a view of the data by month (1=January, 2=February, etc):

A few things to note here:

This data does not capture upside/downside beyond the deal announcement day

Pre and post deal warrant prices have come down significantly on average

December 2021 has been a weak month for post-deal warrant prices

Warrants still seem to exhibit large avg. % increases upon deal announcements

Even in December 2021, 60% of the SPACs which announced deals saw their warrants go up in price. With pre-deal warrant prices down significantly in recent months, one could imagine the forward returns have improved, even if the post-deal pops are not as exciting as they once were. The aggregate data on post deal announcement returns also shows the highest returns on average accrue to warrants trading well below $1.00 prior to deal announcements.

Quick recap before moving on: most pre-deal SPAC warrants currently trade below $1.00, with hundreds trading as low as $0.60 or below. When SPACs get deals done, their warrants tend to trade up well above $1.00 on average, which makes sense when we look at how long term call options are priced using various models. The market is pricing a very high implied SPAC failure rate. If one believes that will not occur then some of these warrants have high return potential.

In Part 2 of this post, I will look at some potential return scenarios and focus on ways to reduce risk through SPAC selection and portfolio diversification.

silly question: what happens if you change the "stock price" input for your black-scholes model to $8 or $6? because current SPAC prices pre-deal-close are kinda "nonsense" in that they include an embedded $10 put (redemption) and the vast majority of deals have traded lower after closing. TIA