Please Step Away From The Ledge

Taking a rational look at financial markets & government intervention

This week the market rallied over 10%, and judging by the reactions online and in various media outlets many people seem to be LOSING THEIR MINDS

All of a sudden people seem pissed off about the Federal Reserve taking action to prevent a depression, and about the state of capitalism generally. Whether it was Chamath Palihapitiya’s widely shared CNBC rant about letting companies fail, the r/wallstreetbets subreddit melting down, or seemingly everyone on Twitter complaining about rigged markets, there’s clearly widespread anger about the stock market and intervention in the economy:

A lot of it sounds like whining from people who were either positioned to profit from a bearish outlook (i.e. the wallstreetbets idiots who have been buying expensive OTM put options on stocks) or people who sat out the recent market rally.

The Barstool Sports guy Dave Portnoy losing millions trying to daytrade this volatile market would be funny if it weren’t so damn sad. It’s turned him into a classic pessimistic permabear who screams about the Fed and puts up awful returns

Dave has been consistently losing money in the past month. He needs some training & education

Many of the permabears were screaming about how the Federal Reserve was “out of bullets” when the central bank cut their benchmark interest rate to 0% in mid March. On the “We Talk Money” podcast on March 18th I tried to dispel that myth. Now these people are **shocked** that the Fed is taking more aggressive actions like lifting some restrictions on banks so they can lend more, helping support fiscal stimulus and loan programs, and even purchasing bonds of companies that have fallen from investment grade status to high-yield (“junk”) status. In the permabears’ eyes, the Fed is wrong and the market is headed for either 1) a crash or 2) hyperinflation, depending upon how the stock market is trading that week. There’s no nuance or middle path.

I saw this same dynamic play out in 2008 and 2009 during the Global Financial Crisis. The permabear viewpoint is seductive, especially to people who are affected by financial crisis and see the injustices in the current economic system. But it is a dangerous one for serious investors looking to grow their wealth over time.

I believe a more rational & nuanced perspective is helpful. Let’s look beyond headlines and take a deeper look at some of the issues at hand. That will provide some needed perspective so we can make decisions that are less rooted in volatile emotions.

Is The Stock Market Detached From Reality?

Thinking that the market (and every stock therein) should trade lockstep with the short term state of economic affairs is naive. If you know anything about equity valuation, then you know that the value of a company and therefore it’s stock is based on the sum of all the company’s future cash flows it will generate for shareholders many years into the future (discounted back to the present by a discount rate that accounts for uncertainty & risk).

That is exactly why a stock’s value (and by extension an index of companies like the S&P 500) is said to be forward looking. Obvious short term events that reduce a company’s cash flows or earnings do matter, but not nearly as much as the long term cash flow generation potential of the underlying business. We know that the economic shutdowns due to coronavirus are severe but also relatively short in nature. Investors must consider what surviving companies will earn when things return to a level of normalcy, particularly in years 2021, 2022, and beyond. So that’s one important factor that can create divergences between the current state of the economy and stock prices.

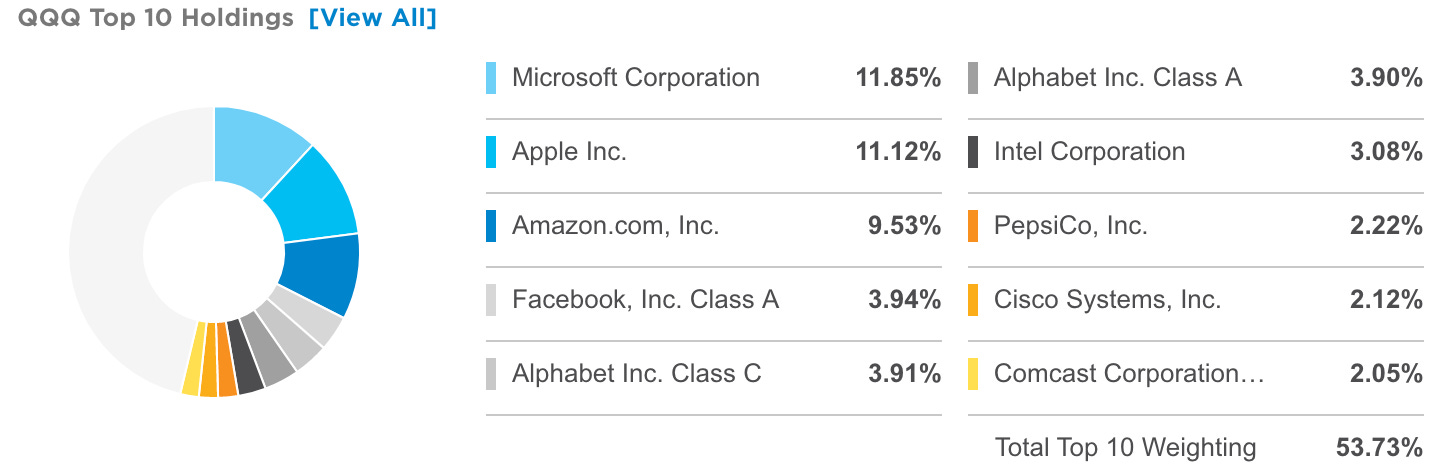

Second, many people measure the performance of the stock market through the performance of broad indexes such as the S&P 500 and NASDAQ 100. But it’s crucial to know that the large well-capitalized tech companies such as Amazon, Apple, Google, Microsoft, and Facebook currently represent a disproportionally large share of the value of these stock indexes. These large tech giants have net cash on their balance sheets to weather the current storm, and some of them such as Amazon and Microsoft are even seeing an increase in some of their businesses (cloud, e-commerce, gaming, etc) during this tough economic environment. These businesses were growing faster than the average business prior to the economic shock as well.

Note the high concentration of big tech in the NASDAQ-100 (QQQ) and S&P 500 (SPY) indexes:

So part of the resiliency of the US “stock market” can be attributed to this concentration. If you look at the year-to-date performance of the Russell 2000 index, which is made up of many smaller companies, it has performed much worse than the S&P500 or NASDAQ-100. The Russell 2000 is still down 25% year-to-date:

Many individual stocks, particularly those in affected sectors such as retail, airlines, hotels, energy, and banking, are still down over 50% year-to-date despite the recent market rally.

It’s also very possible that the stock market as a whole has rallied too quickly and we will see some correction or choppiness in the next couple of months as earnings reports and economic data give investors a better picture of the economic situation and recovery speed. This happened during the GFC as well, with the market initially rallying after the first wave of fiscal stimulus package announcements, before sinking to its final lows in the spring of 2009. Of course we know the market eventually recovered to deliver solid returns over the following decade. Longer time frames provide important perspective!

The Bailout Boogeyman

Now some people will say the market’s recent rise is due to the government “printing money” and company “bailouts”. Let’s address the topic of corporate bailouts first, since the topic is widely misunderstood and also the focus of Chamath’s widely publicized CNBC rant.

I personally dislike the term bailout because it implies a direct, no strings attached transfer of money to companies that never gets paid back. In the vast majority of cases where the US government has provided assistance to distressed companies and industries in the past, the form of that aid has been through loans or senior preferred stock that is paid back with interest. The rescue financing packages usually come with significant stipulations for how the money can be used as well as restrictions on the companies ability to pay dividends and executive compensation. The US government actually generated net profit on its rescue financing programs during the Global Financial Crisis of 2008/2009.

The primary recipients were the eight largest banks (JP Morgan, Bank of America, Goldman Sachs, Morgan Stanley, Citigroup, Wells Fargo, Bank of NY Mellon, and State Street) as well as AIG, Fannie Mae, Freddie Mac, Ally, GM, and Chrysler. Some smaller banks also utilized the TARP programs, but overall very few companies received direct assistance from the federal government. Fannie Mae and Freddie Mac were actually nationalized and the government has been tied up in court for years due to accusations that the government has made TOO MUCH money from those forced takeovers.

Well what about this time around? Chamath was incorrect when he stated that the federal government is bailing out cruise lines. That has not happened yet, and I think that it’s very unlikely cruise lines will receive any assistance from the US government. Royal Caribbean is incorporated in Liberia, Carnival is incorporated in Panama, and Norwegian Cruise Lines is incorporated in Bermuda. The actual ships are registered in various island nations. These cruise ship companies pay very little corporate income taxes to the US government. To bridge them through the crisis period these companies will have to raise debt & equity capital from their own investors. And in fact this is already happening! Just this week Carnival went to market and raised $5.75 billion of expensive debt (11.5% interest rate) as well as $500 million of new equity:

But what about the airlines? The US aviation industry has lobbied hard for the federal government to provide loans and/or grants to keep the airlines from falling into bankruptcy. Airlines have seen revenues plummet 90%, and yet they have significant fixed costs that create massive cash burn while air travel is halted. The CARES Act, the $2.3 Trillion dollar fiscal stimulus bill, includes provisions that will specifically give aid to the aviation industry. One major piece of that aid is $25 billion in cash grants, but those grants are specifically for keeping workers paid and on payroll. It also remains to be seen what strings could still be attached to this money, as the aid package details are still being finalized. There may also be some loans or forced equity stakes required to receive this aid. At the end of the day it’s not going to be a windfall for shareholders of airlines, but it might help some airlines stay out of bankruptcy which does preserve some equity value for current shareholders.

So why do it? Why not let airlines go through the restructuring / bankruptcy process? As Chamath said, the US has a good set of procedures for companies to restructure their debt in bankruptcy. But that is under normal circumstances. In normal times an individual company can go into bankruptcy and if the business is viable, get a Debtor-In-Possession (“DIP”) loan to continue operating while they restructure debt. It is a long and expensive process (lawyer fees charged at $1000 per hour, many negotiations between creditors, court hearings, etc) but it is generally doable. However these are not normal times. Without aid, the entire airline industry would likely fall into uncontrolled bankruptcy AT THE SAME TIME. Our courts probably don’t have the capacity to deal with that, and our commercial banks do not have the capacity (or risk tolerance) to provide $25-50 billion of DIP loans at once to a single industry. Many jobs would be lost and many other downstream businesses (airports, restaurants, hotels, etc) would be permanently harmed. It is better for the government, which has massive balance sheet capacity and low cost of capital (govt bond rates under 1.0%!), to provide needed capital to bridge the airlines through this difficult period.

Look, I get that many businesses (including airlines) should in retrospect have had less debt and more cash to weather a storm. But most individuals and businesses did not plan for a situation in which most of the economy was literally shut down for two months. We have planned for recessions but not this. That probably changes our planning calculus going forward into the future, but it’s the reality we have to deal with now. And the truth is, most of the US federal stimulus IS being targeted at helping small to medium sized businesses as well as individuals who become unemployed/underemployed:

It’s a larger and faster effort than in 2008. I think that’s ultimately a good thing. Why would we want to let the economy spiral into depression? It’s impossible to cleanly clear out weaker companies and create stronger remaining companies during a broad crisis like this. We can argue about the structure of the stimulus programs, and whether individuals should get larger direct payments and certain businesses less. I think Canada actually did a better job than the US at simplifying their assistance programs and getting cash in the hands of individuals rapidly. The US had issues with the PPP program out of the gate which is unfortunate. Bottom line, there are valid criticisms of the fiscal and monetary stimulus programs, but let’s not misrepresent what the goal is here or pretend that we can allow entire industries to fail without serious long term consequences for all of us.

What Happens Next?

So with the economic damage occurring as a result of the virus, the offsetting impacts of stimulus, and financial markets alternating between fear and greed, how do we make sense of it all?

We are dealing with many uncertainties. No one really knows how this will all play out in the short run. But here are some things to think about as we move forward:

Earnings reporting season for Q1 2020 starts up in about two weeks. Prepare for volatility especially in individual stocks. Investors’ focus will be cash burn levels, sources of available capital, and expectations of forward looking demand (signs of/shape of potential recovery)

Will we see a new low in the market again? I can’t say for sure. I do think some stocks may have already seen their low for this cycle. Others still have 100% downside. Understanding balance sheets and liquidity are still VERY important

Should investors go to cash or invest more here? Picking perfect tops and bottoms in the stock market is nearly impossible. The data from multiple studies suggests that trying to be “all-in” or “all-out” is a recipe for poor long term returns. Personally I have some short index hedges and cash reserves but mostly I’m just trying to be patient and scale into (dollar cost average) undervalued companies for the long term. Don’t let daily market movements dominate your emotions and decision making. If I’m a little early on accumulating something that does well over the next 5-10 years it doesn’t matter all that much in the end

Government deficits will be eye popping this year. We are getting our first experiment in broad scale “MMT” style or Basic Income style policies in many countries such as the US. This will shape policy and attitudes about money, deficits, stimulus, etc for many years to come. Whether it leads to inflation/reflation after the crisis depends on many factors. Don’t listen to the fearmongerers calling for hyperinflation. For now there is deflation in the economy offsetting the money created by deficit spending

Expect the backlash against central banks and federal government to continue. This will have implications which may affect elections this year

States are going to be facing some funding crises and this will open up opportunities in industries such as cannabis and gambling

This crisis will also likely lead to more restrictions on companies’ capital allocation. Think less buybacks, dividends, and debt going forward

Watch how hard money hedges such as gold and Bitcoin perform. These may provide uncorrelated sources of return to a broader portfolio

Remember that most human economies & communities find a way to grow and thrive over the long term. We will get through this crisis too

Stay healthy & sane out there! I leave you with an optimistic view on the world:

Thank you, Travis. I always enjoy reading your level-headed, fact-based analysis and insight.