The HUGE Rotation In the Market

And can a tech stock be a value stock?

In my post last week I talked about how bifurcated the market had become between tech/growth stocks and the rest of the market, with tech trading at stratospheric valuations and many other sectors including retail, energy, and financials trading at cheap levels. I had no idea that was about to suddenly shift in a matter of a couple days!

Over the past several trading days we’ve witnessed massive rallies in the formerly beaten up areas of the market while tech stocks have experienced a broad correction. On my watch lists and in my own portfolio I’ve seen some spectacular upward moves in levered companies (those with lots of debt), turnarounds, small caps, retail, energy, and value stocks. This has been very broad based, as evidenced by a chart of the Russell 2000 (small caps) vs the S&P 500 and NASDAQ indices (mid/large caps):

Or a chart plotting the performance of value stocks versus growth stocks over the past several days:

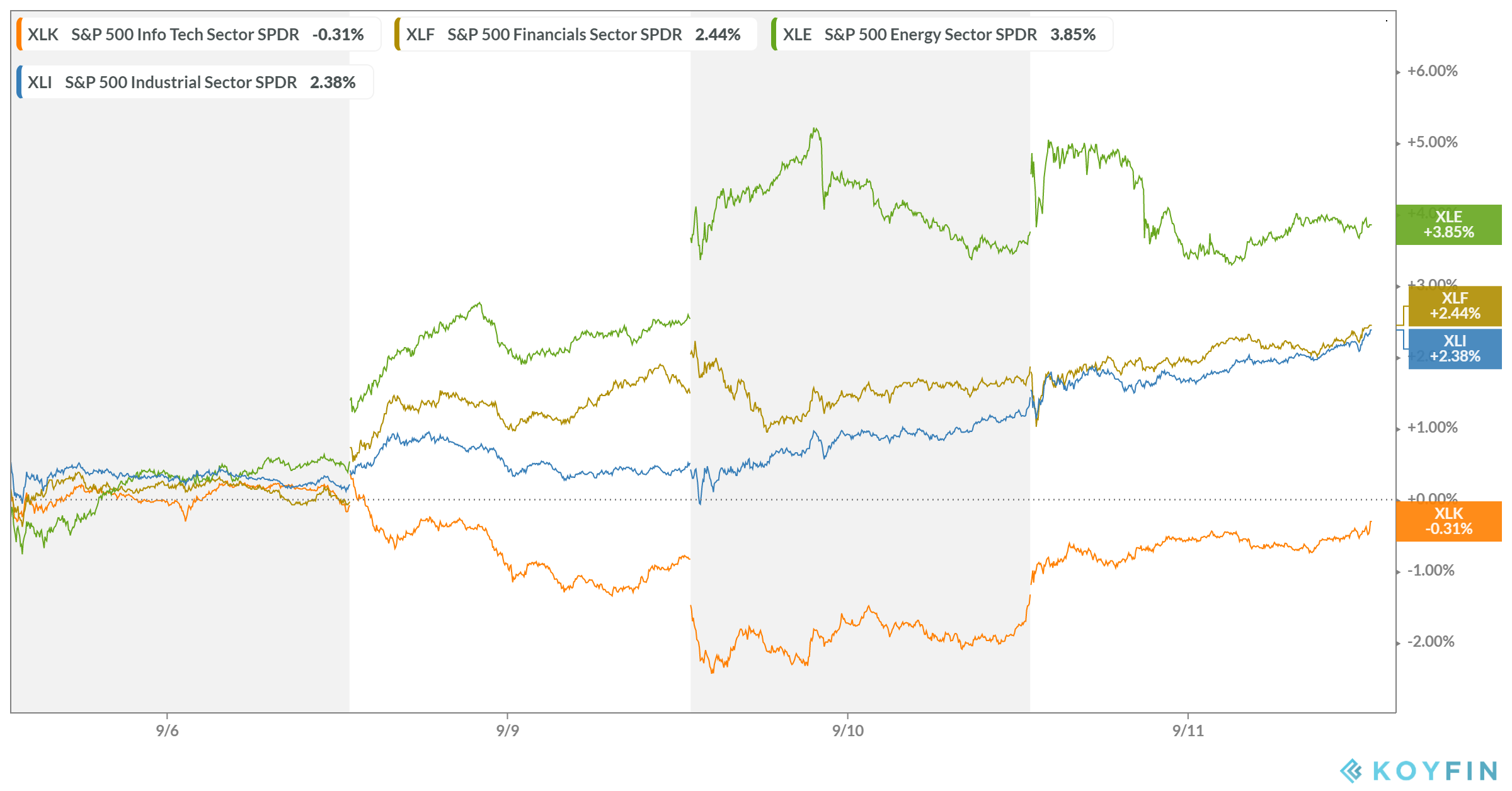

Or a chart of the tech sector versus other sectors such as energy, financials, and materials:

I actually think this is very healthy, especially for tech which seemed overextended & over-owned. Most of the large, popular hedge funds that I follow own the same 20 to 30 stocks, with heavy concentration in tech, SaaS, and payments. This herd behavior increasingly creates latent risk for holders of those stocks if something goes wrong (recall my $ULTA example from last week).

Here you can see the five day performance of some of the high valuation stocks I mentioned last week…it’s not good! 📉

On the flip side, here’s a chart of a handful of stocks that I identified as being interesting risk-reward scenarios in the past few weeks:

The difference in performance is stark!

Some of these companies I’ve tweeted or written about publicly ($DBX, $MCFT, and $ANF for example) and others I’ve talked about privately in my subscription investor community. I identified these well before the market turned. And to be honest, it wasn’t rocket science. It’s just a matter of separating from the herd and making rational & independent judgments, with a very specific focus on identifying asymmetric reward to risk setups.

Where Do We Go From Here?

Now the question is, what happens next? Do I expect this market rotation to continue?

Personally I don’t think the love affair with tech/growth/SaaS is completely over. We’ll likely see some rallies in some of these stocks. But I also think there’s still juice to be squeezed from a lot of the beaten up value plays. I’ve taken some profits on some of my big winners over the past week. However I’m also planning to hold a few of them for long-term multiyear plays.

There’s still a LOT of opportunity in stocks generally right now. Q2 earnings reporting season is mostly over, which means the macro & political environment will dominate market direction until early November. Recession signals and fears probably won’t disappear either, even if the economic data improves a bit with easier comparisons going into late fall. I imagine this could lead to more market-wide whipsaws like we saw in August.

My personal plan is to maintain a solid amount of cash in my active investing portfolio (currently around 35%) both as a hedge against corrections and as dry powder for future opportunities. For me it’s all about finding the irrationality in whatever corner of the market it’s being served up.

Opportunity at the Intersection of Tech & Value?

On to a specific stock that caught my attention today. Lately it’s been hard to find tech stocks that are also reasonably priced, BUT there is such a thing as a value stock within the tech sector once in awhile. Cloudera ($CLDR) might be an example of that, which is a big data software company whose stock was down over 70% from October 2018 through July 2019. Carl Icahn, the famous activist hedge fund manager, filed a 13D indicating he took a new stake in the company around August 1, 2019. Since then, the stock has risen over 50% in just over a month:

Now Cloudera isn’t the subject here (I have no position or opinion on it currently), but I’ve been following another software company stock for the past year that has also had a roller-coaster ride. The company is Domo ($DOMO), which makes BI and data visualization software. Check out the one year chart on this bad boy:

Wowzers. The stock went from $16/share last fall to over $40/share in the spring, but has since sold off all the way back down to mid teen’s levels here in September. It’s in a hot space that has seen two major acquisitions, with Google acquiring Looker for $2.6 Billion and Salesforce acquiring Tableau for a whopping 15.7 Billion. Meanwhile today Domo’s market cap is less than $500 million, and it trades for less than 3X Enterprise Value-to-Revenue while most of its software peers trade north of 8-10X in most cases.

The problem with Domo is that it’s not profitable yet, it’s burning cash, and it’s year-over-year revenue growth rate has decelerated to just 21% in the most recent quarter. It has $133 million of cash on its balance sheet, but also $99 million of debt and it’s burning down its cash pile at a rate of roughly $20 million per quarter currently. The cash burn has been improving a little quarter by quarter and the company keeps saying they will make it to profitability before the current cash runs out, but some analysts aren’t so sure.

I actually put together a very rudimentary forecast model to see if Domo will produce enough cash flow to skirt past any problems in the next couple of years:

Unless revenue growth stops decelerating and/or profit margins rapidly improve, it looks to me like there’s going to be a solvency problem with Domo sometime around the middle of 2021. Now a lot can change before then, and my estimates may certainly be off the mark. Nonetheless, I think it’s important to understand that Domo needs to sustainably generate AT LEAST $50 million of quarterly gross profit to dig itself out of the funding hole (assuming no additional capital gets raised), which is about 75% higher than its gross profit levels today. That means year-over-year revenue growth needs to be above 25% with gross margins at 70%, inconsistent with what we see currently (21% rev growth and 66% gross margin this past quarter).

However, an astute investor & friend of mine pointed out to me that the CEO of Domo, Josh James, spent $1 million of his own money to buy DOMO stock recently. Those kind of large insider buys always get me interested in digging deeper.

🤔 So this one is certainly very puzzling indeed! I clearly need to do a bit more work to understand what the CEO sees that the market and myself do not see. The rewards to getting an edge here could be pretty significant given the volatility and relative valuation discount of this stock.

I’m going to keep hunting through the corrections in tech stocks to see if there’s finally some value emerging somewhere in there. I’d love to find the next $ROKU for 2020! 😎📈