Twitter: Can It Fly Again? 🐦

A breakdown of the social media ugly duckling

It’s earnings season again, so we’re getting a lot of fresh operating & financial data from various companies, and that tends to drive big moves in individual stock prices. One of the more striking moves so far this earnings season was Twitter’s ~25% decline on the back of much weaker than expected earnings:

Oof. Losing nearly a quarter of a company’s market cap in a handful of trading sessions is pretty awful to say the least. Even worse, since Twitter’s IPO nearly six year ago, the stock is only up 15% from the IPO price and is actually DOWN about 30% from where it closed on that first trading day. That is a terrible result for long time public shareholders to say the least.

Contrast that lack of value creation to that of Facebook, another large social media company that went public 7.5 years ago, which has grown its share price about 400% since its IPO:

No wonder Mark Zuckerberg once took a dig at Twitter by calling it a “clown car that fell into a goldmine”! 🤡🤡🤡

However, it’s worth noting that in terms of platform importance and user base, Twitter has likely never been stronger. And the company is increasingly making decisions that diverge from the behavior of other social platforms like Facebook. Just last week, the company’s founder CEO Jack Dorsey announced that Twitter will no longer be accepting political advertising on a global basis:

Political advertising is a meaningful source of revenue for social media platforms, including Twitter, so this will NOT be a good short term move for the company financially. It may however be a great move in terms of user retention and platform health for Twitter given how political advertising has increasingly led to the spread of misinformation, hate, and division among the general populace.

For investors though, the question now is can Twitter ($TWTR) turn things around from a business standpoint? At what level might the stock be a good long term value? Can the company get on the right track and eventually deliver strong returns? This is what I aim to tackle here today.

Twitter: A Brief History Lesson 📚

Why has Facebook done so well for its investors and Twitter done so poorly? The simple and obvious answer is that Facebook’s financial performance has been much better. Facebook has shown tremendous revenue and profit growth, with both growing even faster than the user base. In the past five years, despite growing from a much larger starting base, Facebook has grown annual revenue by nearly 500% compared to 188% five year revenue growth at Twitter. Now Twitter has grown operating profit (“EBIT”) at a faster rate than Facebook in the past five years, but that’s mainly because Twitter was growing off a very small base of profit five years ago. Absolute operating profit at Facebook dwarfs that of Twitter by an astonishing 35X! In addition, EBIT margins at Facebook are nearly double that of Twitter’s.

*Note: EBIT adjustments by Sentieo; figures in USD millions; TTM = trailing twelve months

Facebook also had a more reasonable starting valuation five years ago relative to its future profit generation compared with Twitter. In other words, Twitter’s starting valuation multiple did not do it any favors over this five-year time frame. Adding fuel to the outperformance, Facebook’s share count has grown at less than half the rate of Twitter’s share count over the past five years. That means less of the pie is being taken from shareholders to pay management & employees at Facebook.

What are the underlying drivers of the financial outperformance by Facebook, and the underperformance at Twitter? A number of factors, but a few of them stand out:

Facebook has been MUCH better at acquisitions (Ex: 📸Instagram vs 🌱Vine)

Facebook’s product teams have developed features MUCH faster (Stories etc)

Facebook developed a SIGNIFICANTLY better advertising platform (ad formats, targeting options, reporting, etc)

Facebook’s larger user base naturally attracts more advertisers (scale advantage)

Twitter’s CEO splits his time between two companies ($SQ and $TWTR) while Facebook’s CEO has been laser focused

Facebook’s acquisition of Instagram is particularly notable, with that user base growing over 20X to more than 1 Billion users under Facebook’s stewardship, and an estimated standalone valuation over $100 Billion. It’s been called one of the top corporate acquisitions in recent history. Relative to Twitter, one thing that Facebook has done dramatically better is integration and MONETIZATION of their largest social media acquisitions. Twitter has made promising acquisitions like Vine, TellApart, Periscope, and Magic Pony and then repeatedly failed at doing anything meaningful with them. ByteDance’s TikTok is essentially a more modern version of Vine, and was reportedly last valued around $75 BILLION (3X the current market cap of $TWTR)

Message to Twitter’s highly paid management team 👇👇👇

Swinging and missing on M&A is one thing, because it’s notoriously hard for most companies to succeed with game-changing acquisitions. Failing at product development and advertising platform development however is just inexcusable.

If there’s a slower product team in consumer tech than Twitter’s, I’d be shocked. This is the product team that:

Took YEARS to roll out the basic expansion to 280 character tweets

Took YEARS to double down on the super useful functionality of Lists

Took YEARS to implement features that enhance users’ ability to follow topics (still in testing / limited availability)

Took YEARS to truly address harassment, doxing, and bots on the platform

Still hasn’t added 5-second Tweet editing functionality despite it being a top user request for YEARS

Has not improved the richness or length of user profiles in YEARS

Can’t seem to figure out how to order comment threads in intuitive ways, despite the blueprints they can copy from Facebook

Has made it increasingly difficult to build applications on top of Twitter, despite the company failing to add valuable features themselves

Has strange & arbitrary verification procedures

Has not pioneered the development of any features competitors find compelling enough to copy since the hashtag symbol in 2007

etcetera…

Now that all being said, Twitter remains THE BEST place for people to tap into trending and real-time news. It’s become the de facto global news network, a place where people turn to for breaking news, live sporting events, hot takes, and viral content. Celebrities, politicians, & influencers are increasingly using the platform to amplify their messages and build their followings. Regular people can often engage back with celebs & brands, and even build their professional networks. Journalists use Twitter to source breaking stories and crowdsourced media. And where else could a cult CEO publicly commit blatant securities fraud or a head of state threaten war with just a few keyboard taps? 😳

An argument can be made that the primary responsibility of Twitter’s product organization is to merely not screw all that up. Furthermore, to 💩 on Twitter too hard would be to ignore the strides the company has made in recent years. User, revenue, and profit growth trends have generally been moving in the right direction over the past two years. User base growth has actually accelerated of late:

Twitter stock doubled from January 2017 to January 2019, and kept rising through the middle of this year to over $45 per share ($35 Billion market cap). TWTR’s earnings reports in Q1 and Q2 looked healthy, with year-over-year revenue growth of ~18%, adjusted EBITDA margins in the mid-30% range, and strong free cash flow generation. The company had even shown some discipline on CapEx & expense growth!

The stock went up after both Q1 and Q2 earnings releases, and it looked like Twitter might have finally gained some business momentum. Solid execution, financial discipline, and free cash flow generation leading to stock price appreciation?! Imagine that! 😏

A Disastrous 3rd Quarter 📉

So what the hell happened in Q3 and why has the stock dropped 25% to a market cap in the low $20 Billion range? In short, the numbers were UGLY. Revenue growth suddenly decelerated to just 8% while costs and CapEx spending ballooned, leading to a double digit DECLINE in adjusted EBITDA as well as a ~50% drop in free cash flow compared to the prior year. Making matters worse, management’s excuses for this poor performance were weak and guidance for Q4 suggested continued headwinds. Investor confidence was once again lost.

Classic Twitter.

One of the major headwinds cited by management for the poor results in Q3 was a hit to $TWTR’s mobile app install advertising revenue due to software “bugs” which affected advertisers willingness to spend on mobile app install ads. Management claimed that the company is working on addressing these “bugs”:

However, this was misleading, as these are not truly “bugs” that can be fixed but actually flaws that allowed advertisers to target users incorrectly in the past. That means that this revenue is permanently lost. (See more context here, here, and here)

That was a headwind that apparently cost Twitter three percentage points of revenue growth, but the broader issue is that Twitter is still struggling to improve monetization. Their primary revenue driver is advertising, and they just aren’t attracting advertisers & advertising dollars at a high enough rate. My guess is that many advertisers still aren’t confident enough in the return they can get when advertising on the Twitter platform.

This is an area I know very well, having run the Growth team at a B2C consumer tech startup for four years. My team spent millions of dollars a year on advertising across platforms such as Google, Bing, Facebook/Instagram, Snapchat, Twitter, Spotify, Nextdoor, and others. Performance marketing / user acquisition is all about finding the largest source of users in the target demographic and acquiring those users for as cheaply as possible. Google and Facebook/Instagram attract the majority share of digital ad spending because they have the reach (billions of users) and historically they’ve provided positive return on ad spend for many advertisers. These giants drive the ability for advertisers to obtain positive returns through a combination of factors including:

Very specific intent targeting (Google) or very specific demographic targeting (Facebook/Instagram)

Lots of different ad formats that blend naturally into their products

Clear attribution & reporting so marketers can tie the users who click ads to the conversions that later happen in their apps, websites, or stores

But here’s the thing: these platforms have become increasingly expensive as more and more advertisers spend and compete to acquire the same users. Average cost to reach 1,000 users in developed markets tops $10 on Facebook & Instagram, with a cost per single ad click pushing over $1.00. That may not sound like a lot, but that means a company selling a $100 product needs at least one out of every 100 ad clicks to turn into a sale just to breakeven. On Google, cost per click can easily top $5 or $10 depending on the industry. In competitive industries, digital marketers have driven the cost per acquisition of a user on Google to a level very close to average user LTV (lifetime value), which is the logical long run upper limit an advertiser can tolerate.

Granted, these are proxy metrics that only mildly correlate with cost per acquisition (CPA), cost per conversion, or cost per action which are the metrics that drive advertiser spend in the long run. But assuming conversion rates on Twitter are in the ballpark of those on Facebook/Instagram, it appears that Twitter could be a cheaper advertising option for many advertisers.

Here’s another way to look at it: Twitter’s Revenue per Daily Active User is less than HALF of Facebook’s currently despite Twitter having a higher proportion of highly monetizable US based users (note: the companies don’t report DAU metrics the same way, thus the comparisons aren’t totally apples-to-apples; However, Facebook’s Revenue-per-DAU metric may actually be understated due to the inclusion of Messenger users in DAUs).

So in this environment with increasing digital ad spending and increasing costs for advertisers, Twitter should be an alternative platform that can attract more advertising spend quarter after quarter. This is especially true now that Twitter has a large engaged user base that is actually GROWING at an accelerating rate, which means increasing reach potential for advertisers! It just doesn’t seem like Twitter is executing very soundly on this opportunity right now.

Meanwhile, as revenue growth languishes the company continues to increase headcount and spending, which leads to a decrease in profit and makes the stock look more expensive from a valuation perspective. The selloff is thus not surprising at all.

The Opportunity 💸

It’s easy to be bearish on Twitter. But you don’t drive a car by looking solely in your rear-view mirror. Similarly, great investors don’t make money focusing solely on the past.

How big can Twitter be? What might the shares be worth in a couple of years?

If Twitter could double its Revenue-per-DAU metric, that would translate into more than $3 Billion of incremental annual revenue at presumably very high incremental profit margins. In that scenario Twitter might be able to generate a billion dollars of incremental free cash flow, and that’s before even factoring in a growing Daily Active User count. That might lead to the stock doubling in value or better. The question is, how likely is this to happen and over what time frame?

Management acknowledged the need to improve Twitter’s advertising products on the Q3 earnings conference call. In my opinion, the focus should be on improving the ad formats and courting advertisers by offering better service. Ad load is actually pretty high on Twitter already. Targeting options are reasonably specific with Twitter offering targeting by gender, age, location, keyword, behaviors, followers of specific accounts, as well as re-targeting and custom (“tailored”) audiences. But Twitter still lags behind Facebook and Instagram when it comes to the richness of ad formats.

Facebook and Instagram’s ad formats have more call-to-action (“CTA”) options, allow for richer interactions such as horizontal swiping through image & product card carousels, can roll in the middle of videos, often take up entire screen real estate, and can even be triggered and interacted with through chat messages. You can even book movie tickets from within some of the ads on Facebook & Instagram!

Some example rich ad formats on Facebook & Instagram:

Basic image carousels were tested at Twitter as far back as 2016 but apparently may only soon become a reality here in 2019 or 2020. Ads on Twitter still look pretty basic these days, and the CTAs don’t “pop”, making them less likely to draw clicks for further action. Many ads on Twitter are also odd because the content within the ad is not related at all to the brand running the ad!

There’s no booking movie tickets here…and what do most of these ads even want me to do?

There’s a ton of low hanging fruit just in improving ad formats and calls to action. Twitter’s Explore/Moments section is an ideal place for full screen mobile experiences, along with rich full screen ads, similar to those found on Snapchat and Instagram Stories. A good friend of mine suggested this more than two years ago.

Advertising on Facebook, Instagram, and Google can be extremely frustrating for small advertisers, most of whom are not assigned an account rep or human liaison. Furthermore, Facebook’s advertising platform has become noticeably less stable for advertisers of all sizes in the past two years. As the company has grown more successful they’ve stopped executing like they once did, and this leaves a huge opening for Twitter. If Twitter could figure out how to provide better service to advertisers, that might go a long way in acquiring new clients. Twitter is also under-penetrated in small accounts (“SMBs”), which they’ve admitted as recently as the Q3 2019 shareholder letter:

“By sales channel, large to mid-tier customers continue to represent a sizable majority of our advertising revenue, while our self-serve channel continues to deliver growth off a smaller base”

With its recent ban on political ads and focus on platform health, Twitter is already positioning itself as the good actor within the social media industry. They should use that as a leverage point to gain influence and partners. Partnering with a platform like Shopify, Squarespace, or even Jack Dorsey’s other company Square might be a quick way to accelerate SMB penetration.

In addition, Twitter could reap a lot of benefit by enabling seamless 3rd party transactions from within Twitter. Similar to what I was saying about improving ad formats, Twitter could enable new monetization pathways with “cards” or feed widgets that enable one-click or one-screen Kickstarter/GoFundMe donations, Patreon/Substack subscriptions, Eventbrite/Evite RSVPs, OpenTable reservations, Amazon purchases, Venmo/Paypal transfers, etc. Many of these often already originate on Twitter when users tweet suggestions or requests to their followers. Think this is a crazy idea? This is exactly what Google has done over the past decade with its push to enable flight & hotel bookings, restaurant listings, knowledge panels, maps, and EVEN embedded tweets right there on the Google search page!

Free Call Options? 💰

Meanwhile, with US-China tensions still flaring and TikTok under review by a US Government agency, might there be an opening for Twitter to relaunch Vine🌱? I’m not convinced Twitter has the ability to pull off a sustained comeback here, but it’s worth considering.

What other revenue upside opportunities exist that the stock might not be reflecting today?

Facebook Groups has quietly become a blockbuster product within Facebook, even occupying one of the coveted bottom tray icons in the core mobile app. Many groups number in the 10’s or 100’s of thousands of users, and Facebook is not only serving ads on these pages but also enabling subscription commerce. Reddit is thriving because of its large network of user communities. Paid Slack & Discord groups are also a thing (ex: TrafficThinkTank, NomadList, etc). Similarly, Twitter users are already forming informal communities on the platform (FinTwit is a prime example).

Twitter should figure out how to encourage users to find their tribe and engage in conversation, while enabling creators to make money. Adding the ability to follow interests/topics is part of that, and it’s good to see Twitter finally moving in this direction. The same can be said of Twitter Lists. Perhaps Twitter could acquire Launchpass, Discord, or Substack to move into subscriptions. Like I said before though, Twitter hasn’t been very good at M&A in the past, but there’s $4 Billion of net cash sitting on the company’s balance sheet earning less than 3% annually.

While we’re on the topic of subscriptions: is there a world where Twitter could charge individuals for premium features? Many consumers are increasingly showing an affinity for subscriptions to services like Spotify, Netflix, Amazon Prime, Tinder, YouTube Premium, Stitch Fix, Dollar Shave Club, Dropbox, etc. Even old media companies like the Wall Street Journal and the New York Times are seeing positive subscriber growth. Consumers have finally realized that “if you’re not paying for the product, you ARE the product”. I don’t see why Twitter couldn’t develop and charge for premium features like zero ads, tweet scheduling, one-click tweet promotion, trend monitoring, advanced search & analytics, multiple account management, security enhancements, bio verification, bio videos, etc. They already do much of this through their Premium & Enterprise APIs but perhaps extending it to individual users would be compelling. Companies like Hootsuite and Sprout Social, which may go public soon, have built meaningful businesses providing some of those very services.

There might be other options too, something akin to micro-transactions. When tweets go viral, you’ll often see the author follow up with a link to their Soundcloud or GoFundMe page. As Eugene Wei said, this is a “vulgar monetization hack”. Why doesn’t Twitter try to capitalize on this? Twitch is a great example of a business that built micro-transactions into its product, benefiting both creators and the company.

Twitch users can purchase subscriptions and virtual goods that enhance stream & chat experiences

Tweets are inherently ephemeral, and Twitter prides itself on being the place where real time conversations take place. But there’s also a lot of really cool / valuable things that have been posted on Twitter throughout the years. Why hasn’t Twitter built something that resurfaces the most popular or important Tweets? Or something that allows a user to search for the most bookmarked or pinned content relating to a topic? This might even lead Twitter down the path of becoming a valuable search engine of sorts, which is VERY monetizable given searches typically have high intent (searchers aren’t just mindlessly scrolling a feed).

I don’t particularly like investment theses that depend on some acquirer coming in to scoop up a company at a premium. But as far as free call options go, it’s worth noting that Twitter is a unique asset enjoying improving network effects that has seen potential acquirers surface in the past. Disney, Google, Salesforce, Microsoft, and Verizon have been linked to acquisition rumors previously. It’s also not clear how long investors will tolerate Jack Dorsey remaining at the helm of TWO large companies. Might there be pressure on him to sell Twitter? In my opinion it may be equally likely that Square gets sold, but the dynamic with Dorsey is worth keeping an eye on IMO.

What’s It Worth? 📊

Given the optionality and potential growth levers at Twitter, how should an investor think about the current valuation relative to the company’s future potential?

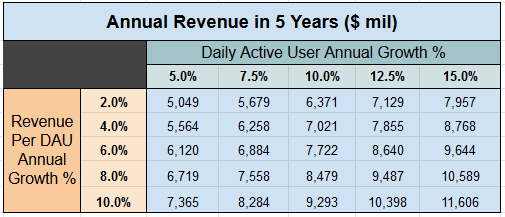

Let’s start with two bullish assumptions about $TWTR: over the next five years the company will 1) increase daily active users (DAUs) and 2) improve Revenue-per-DAU. If one disagrees with these assumptions, it’s very unlikely the stock would look compelling. Here’s what $TWTR’s annual revenue would look like in 5 years under various growth rate assumptions for both DAUs and Revenue-per-DAU:

Even under the most aggressive assumptions here, $TWTR’s revenue-per-DAU metric in five years would be below that of Facebook’s today. The DAU growth assumptions are all below the current growth rate as well. But I’ll stick to the more conservative sets of assumptions and assume Twitter can grow annual revenue to about $7 Billion in five years. That’s a roughly 15% compound annual growth rate (“CAGR”) in revenue, and more in line with Q1 and Q2 of this year than Q3.

Twitter’s Free Cash Flow (FCF) can swing dramatically in a short time span due to the high incremental margins inherent in the business, as well as the pace of capital investment which has historically varied a lot. Twitter appears to be in a heavy investment period, investing both in higher operating expenses as well as CapEx. In fact, CapEx as a % of Revenue doubled in the past two years. Management comments and financial filings suggest heavy data center investments, though it is not clear how much of that is recurring. If I assume 1) Twitter can get CapEx back down to something like 10-12% of revenue and 2) operating expense growth stops outpacing revenue growth, then Twitter’s adjusted EBIT margins could once again reach 30%. That would be in line with management’s target of 40-45% adjusted EBITDA margins:

“there's no change to our thinking that, over time, Twitter can be a 40% to 45% adjusted EBITDA margin business” - Twitter CFO Ned Segal @ Citi Global 2018

With $7 Billion of revenue, 40% adjusted EBITDA margins, and a normalized cash tax rate of ~20%, Twitter might generate close to $1.7 Billion of Free Cash Flow in five years. That’s about a 16% CAGR in FCF from today’s levels. It would be even higher except for the fact that current FCF is inflated since Twitter pays very little in cash taxes at the moment. Due to a history of accounting losses before Twitter became GAAP profitable in 2018, Twitter has a large balance of Net Operating Losses (NOLs) it can use to reduce taxes over the next several years. I typically choose to value NOLs separate from the long-run operating business. There’s about $800 million of present value in Twitter’s tax assets, or roughly $1 per share.

Twitter has about 790 million diluted shares outstanding, though the share count has grown at roughly 4% a year on average over the past three years. Fortunately, the dilution has slowed from egregious to borderline tolerable this year, at roughly 2%. For now, if I assume 2% annual dilution, the share count will be around 870 million in five years.

So that means that $TWTR might be able to generate ~$1.95 in annual FCF per share in five years. Today the average S&P 500 company trades at roughly 20X FCF. Applying that multiple to $TWTR would mean roughly a $40 share price in five years, though that does not include the $5 per share of net cash on Twitter’s balance sheet today or the excess cash $TWTR will generate in the five year period. In fact, it’s likely that Twitter will generate close to $5 per share in additional FCF during the next five years. So Twitter might be worth ~$50 per share in five years. From today’s price of ~$29.50, that would deliver an annualized return of roughly 11% per year over a five year holding period (ignoring unknown impacts from dividends & share repurchases). If you believe the right discount rate for Twitter is 10% then you might conclude that $TWTR stock is slightly undervalued today.

Now it’s also possible that Twitter would deserve a higher FCF multiple than the average S&P 500 company in five years. As any savvy analyst knows, growing companies which sport a Return on Invested Capital (ROIC) greater than their Cost of Capital typically warrant a premium valuation multiple.

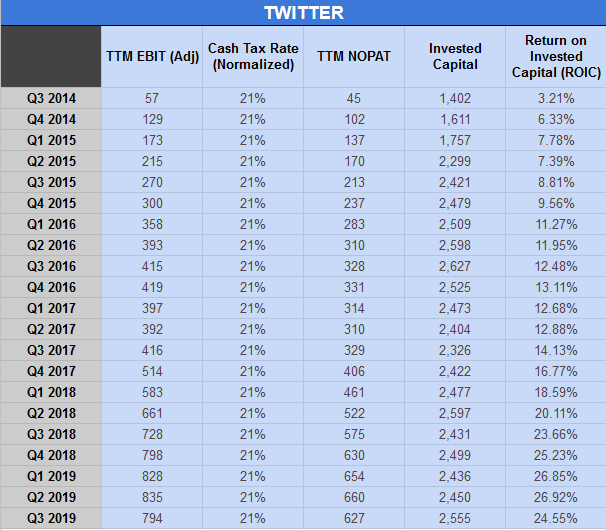

If I normalize Twitter’s abnormally low cash tax rate, here’s what I come up with for Twitter’s ROIC over the past five years:

$TWTR has achieved ROIC in the mid-20% range, which is quite good. As of Q3 2019 however, Twitter’s ROIC is trending down, at least in the near term. Under the five year assumptions I assumed previously, $TWTR’s ROIC would likely rise to >30%. If Twitter still has significant growth opportunities in five years, that level of ROIC would arguably justify an above average valuation multiple, providing further upside to what I mentioned previously.

Valuation is always a tough exercise given the predictions we have to make about the future. As you saw, a proper valuation of Twitter depends on a number of things, including:

Revenue growth drivers such as DAUs and Revenue-per-DAU (monetization)

Incremental profit margins & mature profit margins

Capital Allocation (level/return on CapEx, acquisitions, dividends, buybacks, etc)

Deferred Tax Asset and tax rate assumptions

Value given to excess cash on balance sheet

Share count & dilution

Discount Rate / Valuation Multiple / Valuation Methodology

Final Word on the Bird 🦢

People once questioned Facebook’s ability to monetize mobile, but then the company fixed its product, made successful acquisitions, and became one of the most valuable businesses in the world. Can Twitter prove the critics wrong and do something similar? So many of us see the value & future potential in the product. There were signs in 2018 & 2019 that Twitter was beginning to move faster and produce increasingly exciting features AND financial results. Q3 results were a departure from that, and it seems likely to me that the stock will be volatile in coming months.

Personally, I hope that $TWTR gets it momentum back. I’m also going to be keeping a sharp eye on the stock, because it won’t take that much more of a selloff to bring the stock to levels that I find interesting as an active investor! 🤑

disclaimer: I may own securities mentioned in this publication. I am not a financial advisor and none of this should be construed as financial advice. There’s always risk of loss when investing in stocks. Your investments are your responsibility.